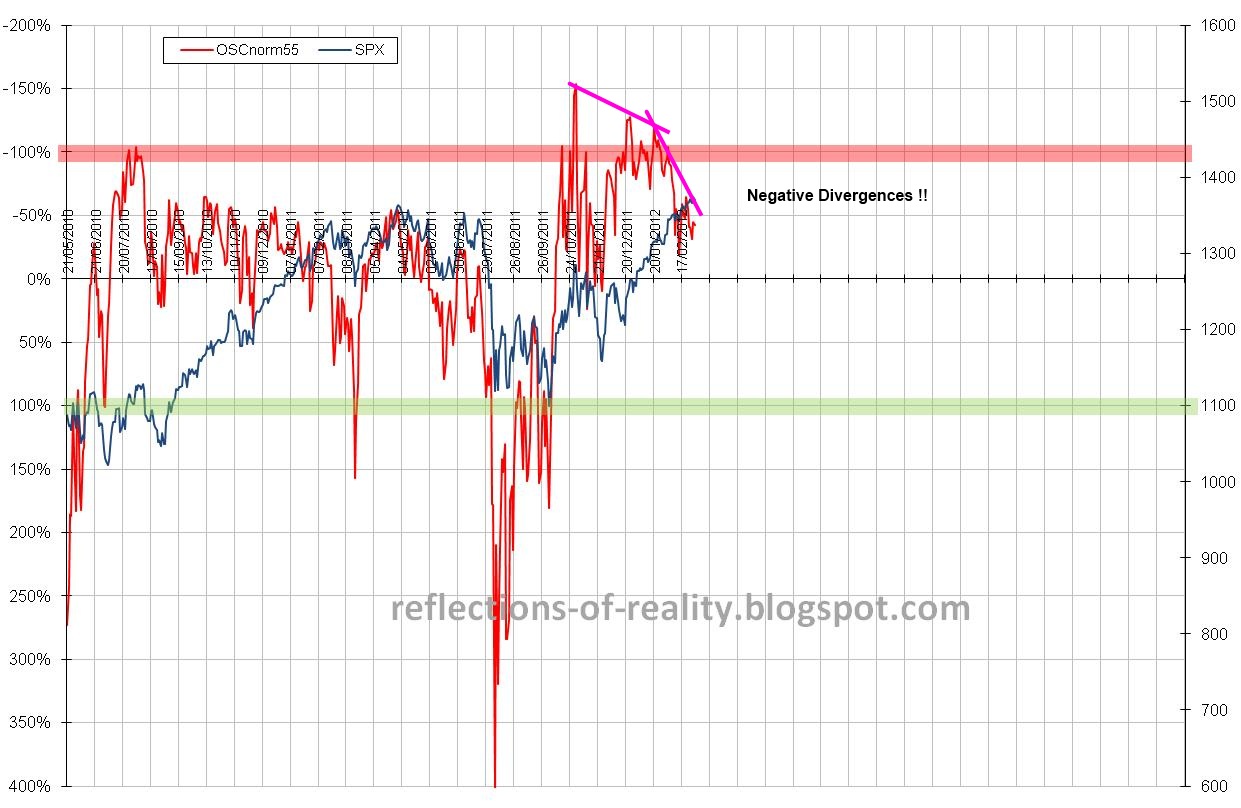

Looking at the CBOE S&P INDEX Options, which are the main vehicle to insure portfolios for long only players, we observe that we have entered the Topping process. At this stage and from this end it is hard to tell how much more 'gas is left' in the Bull's 'tank'.

Our own 'workhorse' VIX Indicators give us the add'l insight that the Topping process is accelerating or spiking as seen from the steeper divergences.....

We feel confirmed with our medium term view that the Market would spike up in Q1, 2012 as a result from LIQUIDITY, LIQUIDITY and LIQUIDITY.

We also still believe that the Bradley Model could be right this year and will not only surprise us with a Spike in Q1 but also with a major move down following mid/late March 2012.

No comments:

Post a Comment